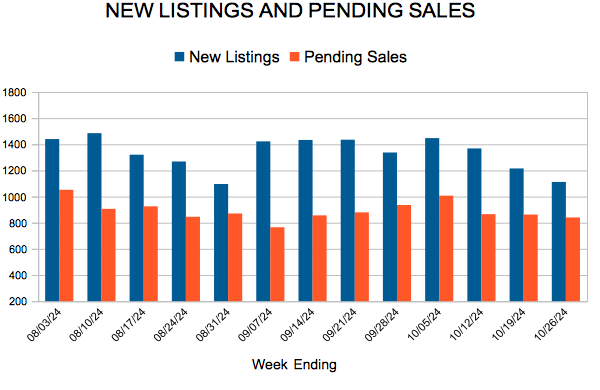

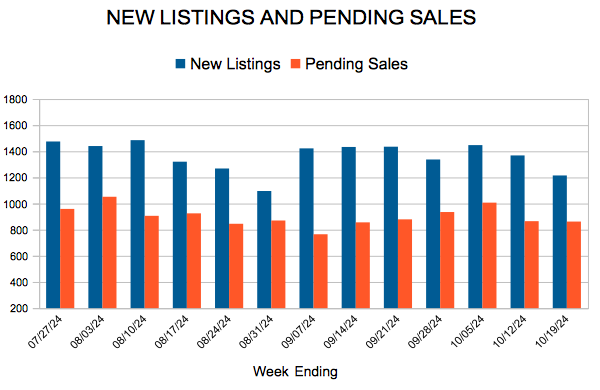

New Listings and Pending Sales

651-770-5000

For Week Ending October 26, 2024

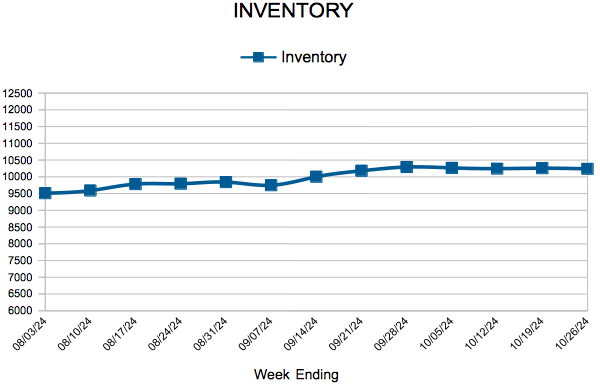

For Week Ending October 26, 2024

Millennials—people ages 28 to 43—make up the largest share of homebuyers nationwide, according to the National Association of REALTORS® 2024 Home Buyers and Sellers Generational Trends Report. Millennials comprised 38% of buyers in transactions that occurred between July 2022 and June 2023, up from 28% the previous 12-month period. Meanwhile, baby boomers, who held the top spot among homebuyers last year at 39%, came in second place, accounting for 31% of all purchase transactions.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING OCTOBER 26:

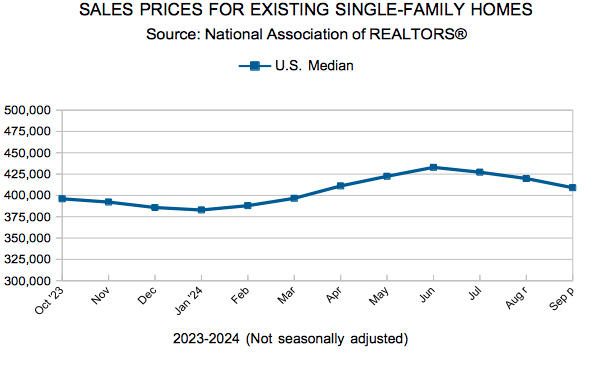

FOR THE MONTH OF SEPTEMBER:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

October 31, 2024

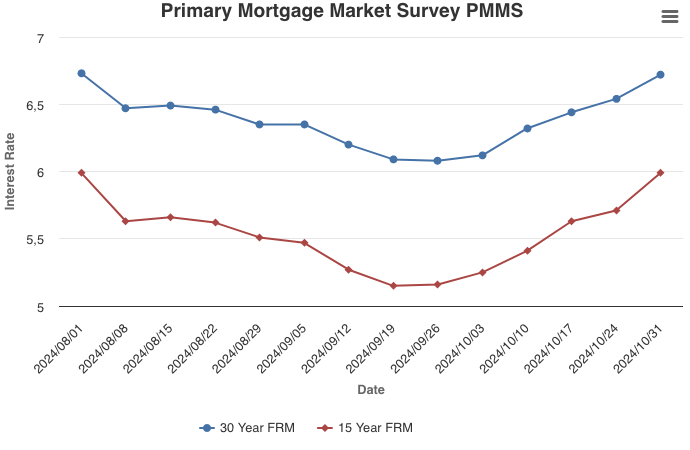

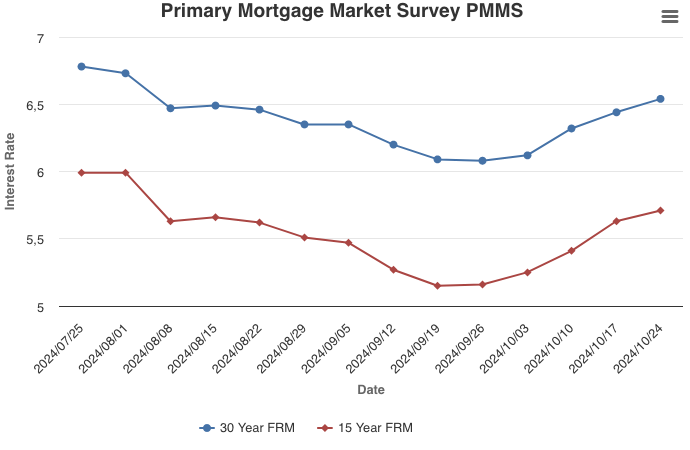

Increasing for the fifth consecutive week, mortgage rates reached their highest level since the beginning of August. With several potential inflection points happening over the next week, including the jobs report, the 2024 election, and the Federal Reserve interest rate decision, we can expect mortgage rates to remain volatile. Although uncertainty will remain, it does appear mortgage rates are cresting, and are not expected to reach the highs seen earlier this year.

Information provided by Freddie Mac.

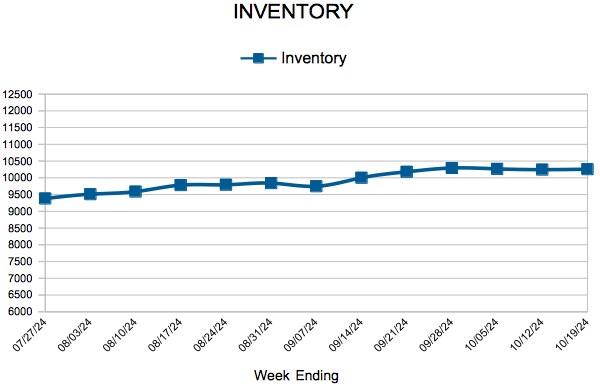

For Week Ending October 19, 2024

For Week Ending October 19, 2024

The number of homes for sale continues to grow nationwide, with Realtor.com reporting there were 34% more homes actively for sale in September compared to the same time last year. This marks the 11th consecutive month of annual growth, with supply now at the highest level since April 2020. Despite the upward trend, however, inventory is 23.2% lower compared to typical 2017 – 2019 levels.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING OCTOBER 19:

FOR THE MONTH OF SEPTEMBER:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

October 24, 2024

The continued strength in the economy drove mortgage rates higher once again this week. Over the last few years, there has been a tension between downbeat economic narrative and incoming economic data stronger than that narrative. This has led to higher-than-normal volatility in mortgage rates, despite a strengthening economy.

Information provided by Freddie Mac.